Student loan debt has exceeded the nation’s credit card debt, according to the Federal Reserve’s G.19 Consumer Credit June report.

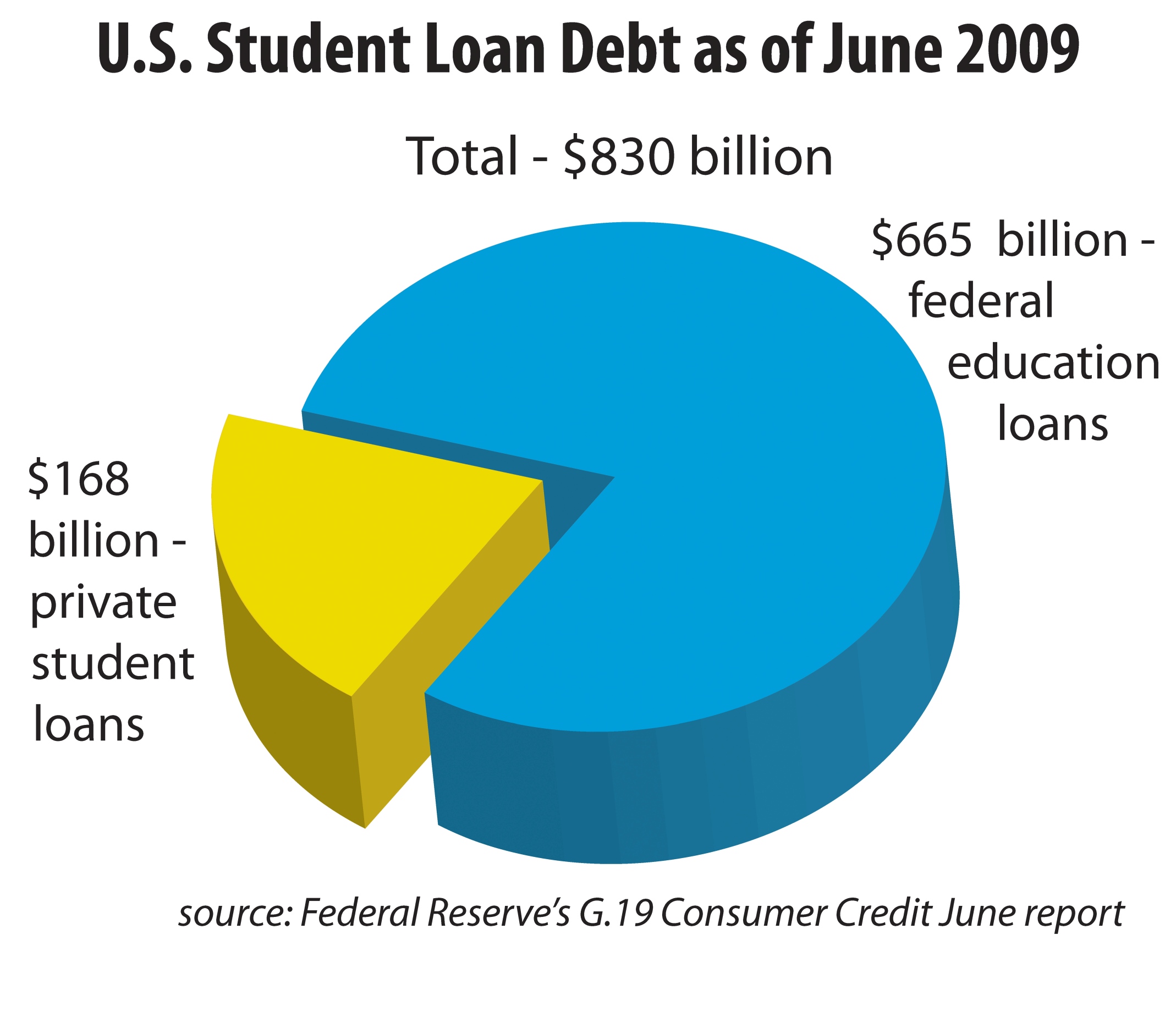

Student debt has reached more than $830 billion — $665 billion from federal student loans and $168 billion from private loans. This total has surpassed the $826.5 billion credit card debt, Mark Kantrowitz, publisher of FinAid.org and Fastweb.com, said in a news release last month.

“There has been significant growth in the total amount of student loan debt outstanding,” Kantrowitz said. “About $300 billion in new student loan debt has been made in the last four years.”

Reserve data show while loan debt has increased, credit card debt has decreased from $838.1 billion in April to $826.5 billion in June.

Amy Marix, associate director of Undergraduate Admissions and Student Aid, said the state of the economy has contributed to the growing debt.

And in the midst of budget cuts and raises in tuition, students are seeking extra assistance.

“[The University] is seeing the need for financial aid increase,” Marix said.

The University currently has 19,910 students on some type of federal, state, athletic or institutional aid, according to the Office of Undergraduate Admissions and Student Aid.

The University distributed $51,949,579 in student Stafford and Perkins loans last year alone.

Another reason for the accumulated debt could be the delay in payment.

“Most students don’t start paying back until they are required to, but you also see a lot of students going to graduate school,” said Emily Burris, coordinator for the Student Financial Management Center.

In the spring 2010 graduating student survey, 31.3 percent of University graduates said they planned to attend graduate or professional school full time.

Burris said many students wait because they have the option to defer payment until after graduate school.

Psychology freshman Angelle Kerek is one of those students. All of Kerek’s schooling is paid for through financial aid while loans cover her living expenses.

“I got my loans so I could have a place to live,” Kerek said. “I plan on paying them off either after graduation or after graduate school — probably after graduate school if I have a real career by then.”

The standard repayment term on student loans is 10 years, but students have the option to consolidate or extend loans to a 20- to 30-year repayment schedule, Marix said.

Student loans have both advantages and disadvantages, Burris said.

“Student loan debt is what they call good debt,” Burris said. “Getting a college degree is worth it, specifically a degree from LSU.”

Marix agreed student loans are a good option if needed for college but said students should only borrow what they absolutely need.

This “wants versus needs” agenda is one Burris teaches to students.

“If students are looking for ways to finance while in school, keep a budget,” Burris said. “See exactly what you are spending, and see where you can cut back. Whenever you put it down on paper, you can see what areas you can make sacrifices in to avoid a massive amount of debt.”

Burris said managing finances this way will help alleviate stress and prepare students for the future.

“Before a student takes out a loan, they need to talk to Financial Aid,” Burris said.