Shannon Schuyler

Principal, Chief Purpose Officer and Corporate Responsibility Leader at PwC and President of PwC Charitable Foundation

My young colleague Gabi has a great career ahead. She graduated from a first-rate university last year with a double major and double minor in high demand fields. She interned with PwC starting in her second year of college, taking on progressively sophisticated roles each summer, and transitioned to working with us as an associate immediately after graduation. Gabi’s a smart, competent young adult who has managed many challenges successfully. She immigrated to the United States from Chile with her parents and older sister when she was seven. But like most of her peers—millennials who will comprise more than 75 percent of the workforce by 2025—Gabi is worried about money.

Gabi is a typical millennial in many ways. She graduated from college with long-term debt (student loans and a car payment) and experiences considerable stress around meeting monthly expenses. Something else Gabi has in common with her peers—she received very little financial education (one week in a high school math class) before choosing to study accounting in college.

Millennials are on course to become the most educated generation in American history. But they face greater economic challenges than previous generations and are already financially fragile. A study our firm released this month, Millennials & Financial Literacy—The Struggle with Personal Finance, conducted by The Global Financial Literacy Excellence Center (GFLEC) at the George Washington University with the support of PwC, found that students like Gabi aren’t alone. In fact, a wide majority of millennials are struggling to understand fundamental financial concepts and manage their debt. Among the findings:

– Only 24% of millennials demonstrate basic financial knowledge.

– The majority of millennials carry long-term debt. 55% of college graduates have student loans, including 34% of young adults with annual incomes of more than $75,000.

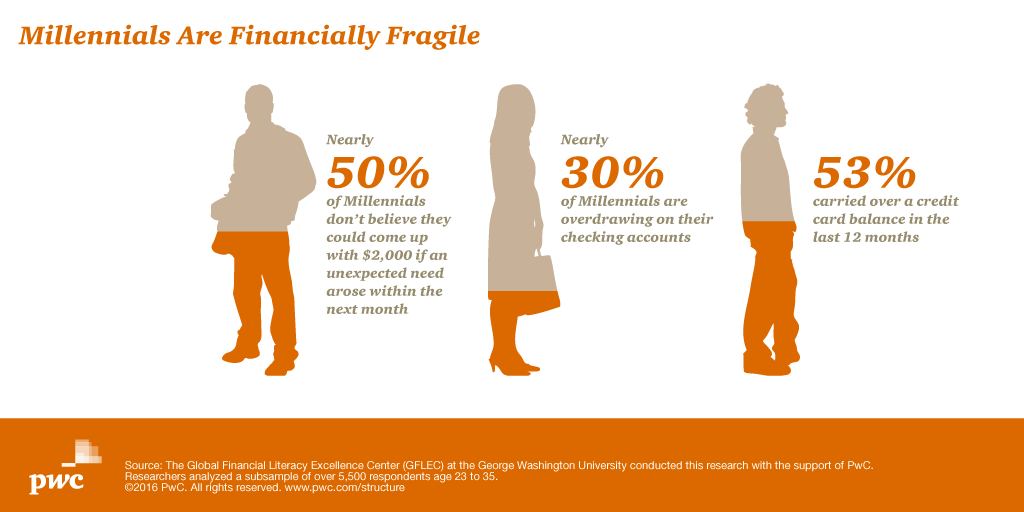

– More than half of millennials carried over a credit card balance in the last 12 months and 45% make only minimum monthly payments.

– Millennials are unprepared to weather a shock. Nearly half say they could not come up with $2,000 within the next month to meet an unexpected need.

Despite the fact that millennials are facing these issues in large numbers, the study found that they are afraid to ask for help. In fact, a startling few (27%) seek professional financial advice. Financial literacy is such a pervasive issue for this generation, and it’s important to know that it’s okay to ask for help.

The gap is widening between the amount of financial responsibility given to young Americans and their demonstrated ability to manage personal finances. It’s time to reduce that gap. Young people must be empowered to make smart financial decisions, because the economic stability and success of our businesses and communities depends on their choices.

In 2012, my firm launched its Earn Your Future (EYF) commitment focused on helping young people develop critical financial skills and providing educators with resources and training to teach financial literacy. In 2015, we extended our commitment, now totaling $190 million. We don’t have all the answers, and our efforts will continue to evolve. Still, I am optimistic. A few months ago, I met with an exuberant group of third-and-fourth graders participating in an EYF program. I asked if they thought it was better to spend on a toy or a game that they wanted now or to save for the future. In unison they shouted “save!” These kids have something in common with Gabi.

Unlike many of her peers (perhaps because she studied finance in college or because of her family’s experience), Gabi is saving rather than spending—for now, she has chosen to live at home with her parents in order to pay off her student loans more quickly—and she is learning about ways to boost her credit score. She also reaps benefits from working at PwC, which this past year announced a student loan pay down program to help reduce student loan burden. But all adults, regardless of education or employer, should be able to manage their personal finances. Expanded access to financial education can bring powerful improvements in financial literacy and financial stability for the next generation of Americans.

For more information on millennials and financial literacy, visit pwc.com/us/millennialsfinlit.

Media Contact

Sarah Tropiano

PwC

(703) 307-3823

sarah.b.tropiano@pwc.com